Richard Germain is a Managing Director at MA Financial Group. Richard helps manage and grow the Real Estate Asset Management business which includes sourcing appropriate fund investments and investment capital, both institutional and high net worth and the establishment and investment management of real estate funds and assets. Richard was previously an investment advisor and portfolio manager at Lend Lease Corporation Limited including providing portfolio management, product design, and advice to the company’s funds on appropriate investment.

Real estate has proved to be one of the most resilient and best risk adjusted performing investment classes in Australia since the early 1900’s.

Retail real estate in particular offers investors an attractive counter-cyclical investment opportunity, underpinned by a range of strong underlying trends.

Long history of consistent and resilient retail sales growth

The sector has been underpinned by a long history of consistent, resilient and solid growth in retail sales.

Over the past five decades or more, the Australian Bureau of Statistics have not recorded a single year of negative retail expenditure growth – including during periods of economic uncertainly.

In the 12 months to December 2020 retail expenditure grew 10% despite significant COVID-19 related disruptions. During the global financial crisis retail expenditure grew on average 12% p.a. between 2007-2009, despite increasing unemployment and sharp corrections in equities markets.

People and food the key drivers

Australia’s high population growth has been a catalyst for this increase, and has supported non-discretionary retail categories such as food in particular.

Since 1982, ‘Total Food Retailing’ and ‘Total Cafes, Restaurants and Other Takeaway Food’ have delivered the highest average annual growth rates of 6.3% and 6.6% p.a., respectively.1

Australian shopping centres, anchored by national supermarket retailers such as Coles and Woolworths, account for a significant portion of total retail sales.

Low supply, high barriers to entry

The Australian retail market exhibits very different characteristics to other retail markets around the world, in large part due to the high barriers to entry but also comparative low supply versus the major markets of North America.

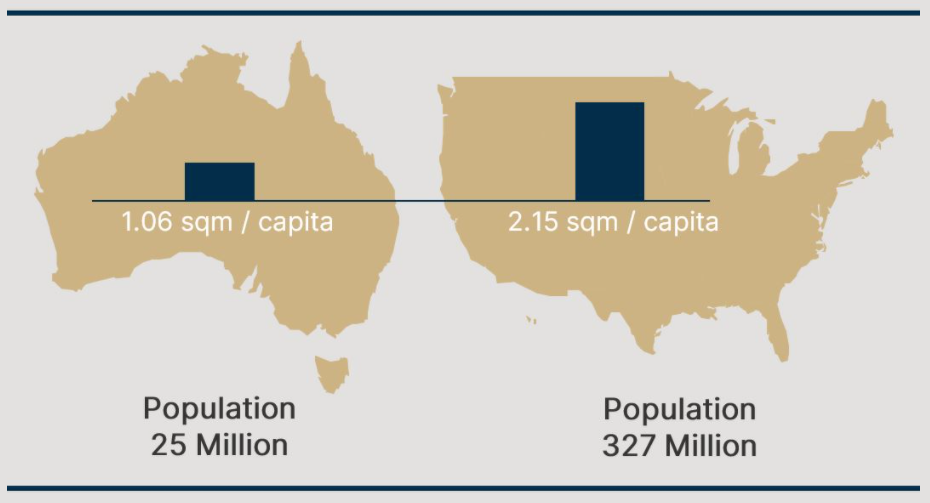

Less than half the supply of the US

Australia has retail supply of approximately 1.06sqm per person compared to the US which has more than double this.

Retail space provision - Australia vs United States

Restrictive zoning regulations

In Australia, the supply of new retail floorspace per additional person has been decreasing – from 2.6sqm p.a. in 1995-1999 to 1.1sqm p.a. between 2015-2019.

This reduction can be attributed to the fact the supply of new retail floorspace in Australia is tightly controlled by restrictive zoning regulations, and our high population growth has led to greater emphasis on residential planning schemes.

This restricts the ability to develop new retail shopping centres in established metropolitan areas, meaning new retail supply is often introduced into high residential growth areas along the metropolitan periphery which has no material long-term impact on established shopping centres.

High occupancy rates, diversified tenant base

Occupancy rates for Australian retail assets are high, with a national average vacancy rate of only 6.9% and a 10-year average of 4.2%.2

Retail assets are assisted by the diversity of their tenant base. While Australian shopping centres are generally anchored by the major supermarkets and often discount department stores, the sub-regional and regional centres also have a diverse range of smaller tenants reducing the exposure to any individual tenant.

Strong and resilient Australian economy

The strength in the retail sector is supported by a strong and resilient Australian economy.

Until the exceptional circumstances brought on by COVID-19 in 2020, Australia had not experienced a recession since 1991.

The economy has been driven by strong population growth, increasing productivity and access to in-demand natural resources. It remains a highly desirable destination due to our favourable standards of living, including a top tier medical system, stable governance and strong agricultural production.

The sector is well positioned to continue on an upward growth trajectory and is increasingly being sought by institutional investors.

This article was originally published by M A Financial. Read it here…